" width="117.18528112673562px"><path d="M 2.921 9.684 L 0 4.89 L 2.674 0 L 2.73 0 L 5.786 4.698 Z" fill="rgb(255, 255, 255)" height="9.68390559853665px" id="WVz_1otEz" transform="translate(13.924 0.603)" width="5.785774342577639px"/><path d="M 3.128 0 L 3.197 0.106 L 6.254 4.805 L 6.331 4.925 L 3.198 10.378 L 0.071 5.246 L 0 5.13 L 2.739 0.122 L 2.806 0 Z M 0.541 5.118 L 3.186 9.458 L 5.782 4.94 L 2.987 0.644 Z" fill="rgb(236, 236, 228)" height="10.378179230817523px" id="pWwexydgS" transform="translate(13.683 0.362)" width="6.331283661760494px"/><path d="M 27.976 0 L 31.089 4.699 L 19.439 24.739 C 19.106 25.315 18.406 26.212 17.474 26.833 C 16.8 27.281 16.007 27.585 15.143 27.52 C 13.997 27.488 11.495 26.887 10.656 24.739 L 0.247 6.616 C 0.112 6.18 0.032 5.729 0.009 5.273 C -0.087 3.546 0.548 1.271 3.494 0.384 L 16.289 0.384 L 13.711 5.273 L 16.57 9.972 L 15.054 12.542 L 13.559 9.972 L 17.855 17.356 L 27.881 0 Z" fill="rgb(0, 44, 21)" height="27.528638004930308px" id="S8lzwCbyW" transform="translate(0.241 0.241)" width="31.088708222788753px"/><path d="M 28.336 0 L 28.406 0.105 L 31.518 4.804 L 31.599 4.925 L 31.526 5.051 L 19.877 25.091 L 19.876 25.09 C 19.551 25.652 18.896 26.503 18.016 27.139 L 17.838 27.263 C 17.136 27.729 16.292 28.058 15.36 27.988 C 14.757 27.97 13.818 27.805 12.917 27.368 C 12.012 26.93 11.126 26.209 10.677 25.072 L 0.278 6.967 L 0.265 6.944 L 0.258 6.92 C 0.117 6.465 0.034 5.995 0.009 5.521 L 0 5.178 C 0 4.365 0.166 3.458 0.642 2.631 C 1.189 1.68 2.135 0.853 3.66 0.394 L 3.693 0.384 L 16.911 0.384 L 14.214 5.499 L 17.005 10.084 L 17.077 10.204 L 15.56 12.776 L 18.088 17.122 L 27.98 0 Z M 0.498 5.742 C 0.532 6.087 0.598 6.428 0.699 6.76 L 11.094 24.857 L 11.102 24.871 L 11.108 24.888 C 11.5 25.891 12.283 26.541 13.121 26.946 C 13.856 27.302 14.621 27.463 15.165 27.508 L 15.384 27.52 L 15.395 27.52 L 15.544 27.528 C 16.21 27.543 16.833 27.324 17.392 26.988 L 7.66 9.972 L 13.928 9.972 L 15.289 12.312 L 16.53 10.207 L 13.813 5.742 Z M 18.09 18.058 L 15.287 13.24 L 15.086 12.895 L 13.659 10.441 L 8.467 10.441 L 17.783 26.728 C 18.577 26.142 19.177 25.365 19.471 24.856 L 31.047 4.941 L 28.173 0.602 Z M 3.764 0.852 C 2.364 1.282 1.528 2.03 1.048 2.864 C 0.605 3.636 0.459 4.497 0.471 5.273 L 13.803 5.273 L 16.134 0.853 L 3.764 0.853 Z" fill="rgb(236, 236, 228)" height="27.997745133258043px" id="K78MR2kAx" width="31.598913805263862px"/><path d="M 12.817 0 L 2.76 17.463 L 0 12.566 L 7.394 0 Z" fill="rgb(195, 245, 60)" height="17.462808255781656px" id="RvrsdZNfk" transform="translate(15.25 0.241)" width="12.817479921596572px"/><path d="M 13.493 0 L 3.027 18.171 L 0 12.798 L 0.068 12.682 L 7.531 0 Z M 0.54 12.804 L 3.032 17.223 L 12.682 0.469 L 7.799 0.469 Z" fill="rgb(236, 236, 228)" height="18.170583997353802px" id="wbm2UXp6F" transform="translate(14.949 0)" width="13.492947034089838px"/><path d="M 1.844 5.288 L 6.505 15.096 C 6.768 15.652 6.742 16.419 6.742 17 L 7.137 17 C 7.137 16.392 7.11 15.652 7.374 15.096 L 12.009 5.288 L 13.852 5.288 L 8.058 18.508 L 5.925 18.508 L 0 5.288 Z M 15.569 2.115 L 15.569 0 L 17.676 0 L 17.676 2.115 Z M 15.727 18.508 L 15.727 5.288 L 17.57 5.288 L 17.57 18.508 Z M 22.804 6.53 C 23.936 5.182 25.043 4.892 28.018 4.892 L 28.018 6.662 C 25.016 6.662 22.146 7.615 22.146 11.289 L 22.146 18.508 L 20.302 18.508 L 20.302 5.288 L 22.146 5.288 L 22.146 6.319 C 22.146 6.953 21.829 7.72 21.619 8.328 L 21.987 8.46 C 22.198 7.852 22.382 7.033 22.804 6.53 Z M 31.965 17.477 L 31.965 25.118 L 30.121 25.118 L 30.121 5.288 L 31.965 5.288 L 31.965 6.24 C 31.965 7.033 31.622 7.984 31.359 8.751 L 31.727 8.857 C 31.991 8.116 32.202 7.059 32.755 6.504 C 33.755 5.499 35.125 4.892 36.915 4.892 C 40.865 4.892 43.42 7.879 43.42 11.818 C 43.42 15.758 40.865 18.931 36.915 18.931 C 35.125 18.931 33.729 18.296 32.755 17.212 C 32.202 16.63 31.991 15.573 31.754 14.832 L 31.359 14.964 C 31.622 15.705 31.965 16.683 31.965 17.477 Z M 36.915 6.662 C 33.65 6.662 31.965 8.91 31.965 11.818 C 31.965 14.727 33.65 17.159 36.915 17.159 C 40.154 17.159 41.576 14.727 41.576 11.818 C 41.576 8.91 40.154 6.662 36.915 6.662 Z M 43.59 11.818 C 43.59 7.879 46.408 4.892 50.384 4.892 C 54.334 4.892 57.152 7.879 57.152 11.818 C 57.152 15.758 54.334 18.931 50.384 18.931 C 46.408 18.931 43.59 15.758 43.59 11.818 Z M 45.433 11.818 C 45.433 14.726 47.118 17.159 50.384 17.159 C 53.623 17.159 55.309 14.727 55.309 11.818 C 55.309 8.91 53.623 6.662 50.384 6.662 C 47.118 6.662 45.433 8.91 45.433 11.818 Z M 58.599 2.115 L 58.599 0 L 60.705 0 L 60.705 2.115 L 58.599 2.115 Z M 58.757 18.508 L 58.757 5.288 L 60.6 5.288 L 60.6 18.508 Z M 66.123 6.028 C 67.414 4.97 68.546 4.892 70.495 4.892 C 73.233 4.892 75.341 6.424 75.341 9.439 L 75.341 18.508 L 73.497 18.508 L 73.497 10.761 C 73.497 7.826 72.364 6.53 69.968 6.53 C 67.361 6.53 65.175 7.852 65.175 10.761 L 65.175 18.507 L 63.332 18.507 L 63.332 5.287 L 65.175 5.287 L 65.175 5.631 C 65.175 6.424 64.78 7.376 64.491 8.09 L 64.859 8.248 C 65.149 7.535 65.517 6.556 66.123 6.028 Z M 80.092 15.308 L 80.092 7.139 L 77.458 7.139 L 77.458 5.367 L 80.092 5.367 L 80.092 1.19 L 81.935 1.19 L 81.935 5.367 L 85.359 5.367 L 85.359 7.139 L 81.935 7.139 L 81.935 15.308 C 81.935 16.419 82.436 16.736 83.673 16.736 L 85.228 16.736 L 85.228 18.508 L 83.12 18.508 C 81.33 18.508 80.092 17.265 80.092 15.308 Z" fill="rgb(0, 44, 21)" height="25.117542346525326px" id="X8ixUchOP" transform="translate(31.826 4.882)" width="85.35888418459695px"/></g></svg>)

Finance

Volatility Index Signaling Complacency Into Year-End

Darren Reed

Dec 24, 2025

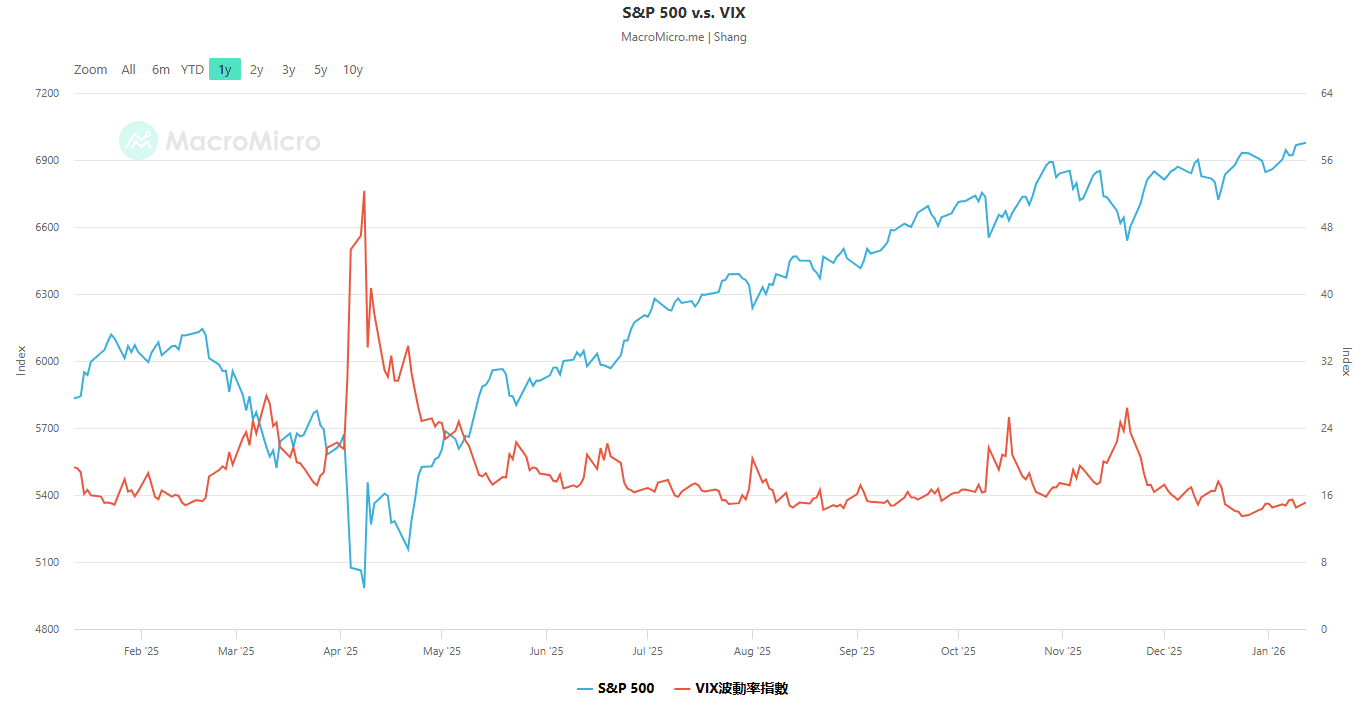

What the VIX Is and What It Measures

The Cboe Volatility Index (VIX) is often called the market’s “fear gauge,” but it’s more precise to view it as the price of short-term insurance on the S&P 500. The VIX represents the market’s expectation of volatility over roughly the next 30 days, inferred from the implied volatility embedded in a broad strip of S&P 500 index options. When investors pay more for protective options, implied volatility rises and the VIX tends to increase. When demand for protection fades, implied volatility compresses and the VIX generally falls.

Why the VIX Often Moves Inversely to the S&P 500

Because it is derived from option prices, the VIX commonly trades inversely to the S&P 500. During equity drawdowns or risk-off shocks, investors rush to hedge downside risk—often by buying put options—driving up option premiums and implied volatility. The VIX rises as that “insurance” becomes more expensive. In risk-on periods, when equities trend higher and dips are quickly bought, hedging demand tends to ease and volatility sellers may add supply, helping push implied volatility (and the VIX) lower. The relationship isn’t perfect day-to-day, but over time the negative correlation is a frequent feature of how the index is constructed and used.

All-Time Highs and Compressed Volatility

A relatively low VIX compared with historical averages fits neatly with U.S. equities trading at or near all-time highs. When the S&P 500 is strong, realized volatility often stays subdued: pullbacks are smaller, sentiment is steadier, and investors feel less urgency to pay for protection. This can become self-reinforcing. As volatility remains contained, certain systematic strategies that adjust exposure based on volatility levels may keep or add to equity exposure, contributing to smoother price action. At the same time, consistent demand for yield-like returns from option premium selling can further suppress implied volatility.

Year-End Seasonality and the Christmas Rally

Seasonality can amplify this calm. The final weeks of the year are widely associated with the “Christmas rally,” when holiday-thinned trading, portfolio positioning, and generally optimistic sentiment can support equities. In a slow grind higher—rather than a choppy tape—implied volatility often compresses. With fewer perceived catalysts into year-end and many investors reluctant to make big reallocations during the holidays, the market’s willingness to pay for near-term insurance tends to soften, keeping the VIX muted relative to its long-run average.

A Low VIX Isn’t the Same as Low Risk

A low VIX describes how the market is pricing near-term uncertainty today—not a guarantee that uncertainty won’t spike tomorrow. If a surprise catalyst hits (a macro data shock, an abrupt shift in rate expectations, geopolitical escalation, or a sudden liquidity event), the VIX can reprice quickly. Historically, volatility tends to be mean-reverting: long quiet periods can give way to sharp bursts, and the VIX can move far faster than equities in stress regimes.

Bullish VIX Outlook and the ETF Angle

With the VIX trading historically low, a “bullish VIX” view is essentially a bet on volatility mean reversion: the idea that complacency and compressed option premiums leave room for an eventual repricing higher. In practical terms, when insurance is cheap, the asymmetry can look attractive—there may be more room for a volatility spike than for volatility to fall much further, especially if equities are already extended at all-time highs and seasonality fades into the new year.

It’s also important to connect this to how many popular VIX-linked ETFs and ETNs (e.g. VIXY and VXX, respectively) behave. Most are not direct, long exposure to the spot VIX; they typically gain exposure through VIX futures. When volatility rises, those products often rise as well, and can do so sharply during sudden spikes. However, their performance is heavily influenced by the shape of the VIX futures curve. In “contango” (when longer-dated futures are priced above near-dated), long VIX ETPs can experience significant drag over time from rolling futures forward—meaning they are generally better suited for tactical positioning around an anticipated volatility event rather than long-term holding. Still, for investors looking for convexity—a potential surge in payoff during an equity shock—low spot volatility levels can be the kind of backdrop that makes volatility exposure feel compelling, provided the risks and mechanics are well understood.